Making Tax Digital for Landlords: Preparing for April 2026

Time to read: 6 mins

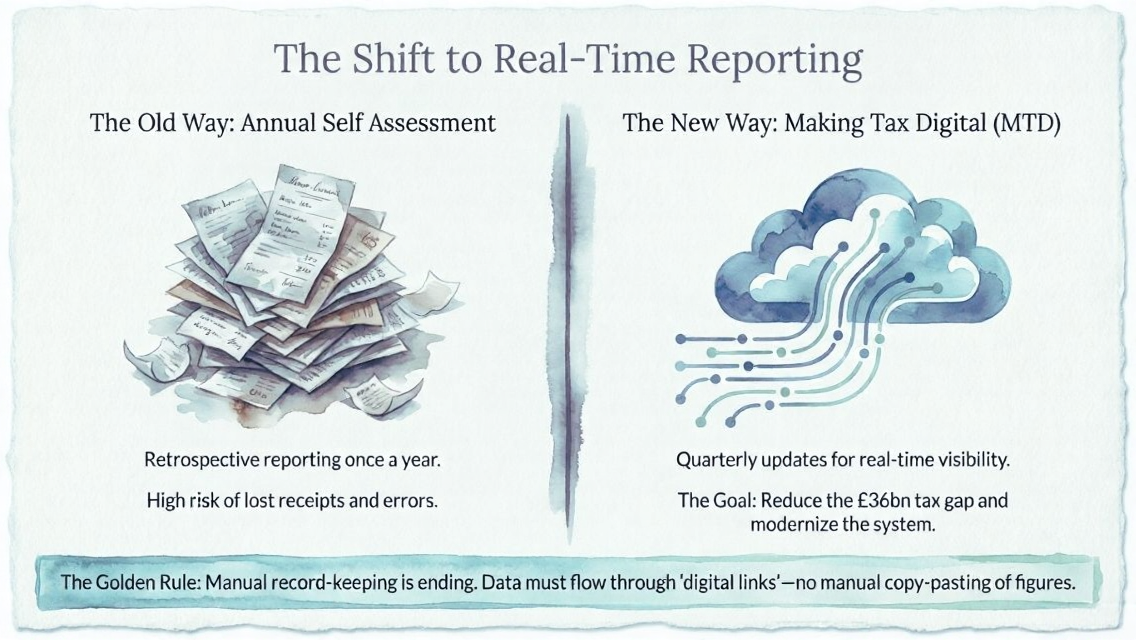

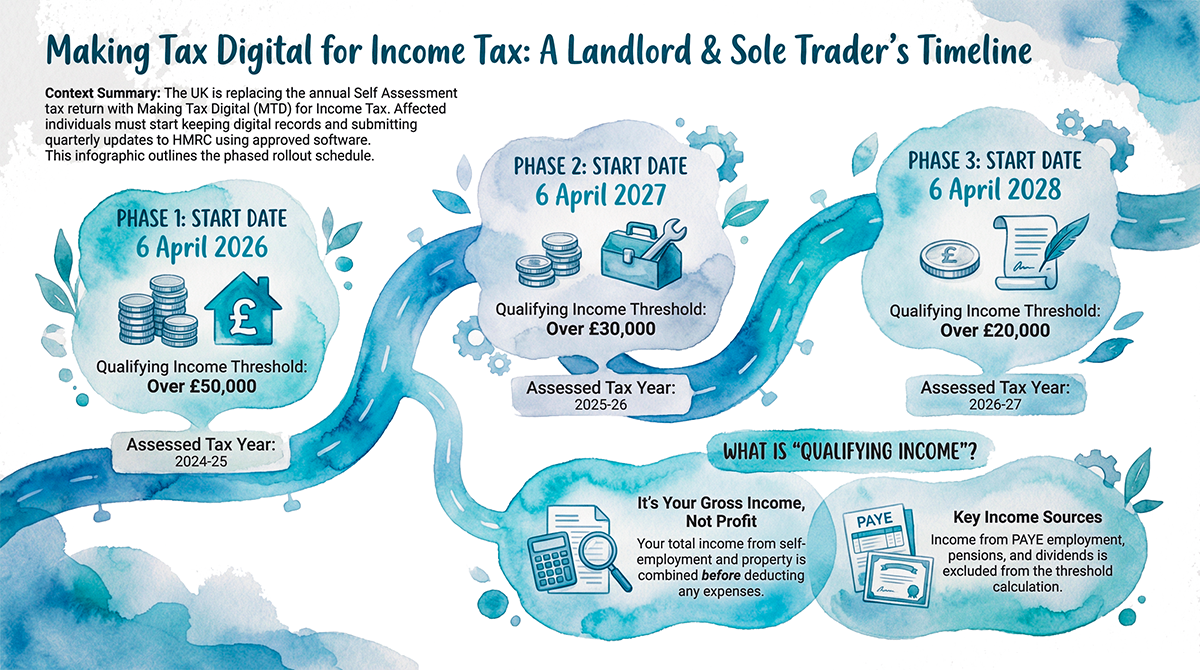

Making Tax Digital (MTD) is the UK government’s shift to digital tax reporting. It started with VAT. It is now extending to Income Tax Self Assessment. For residential landlords, the operational shift begins on 6 April 2026.

From that date, landlords with total gross rental or self-employment income above £50,000 must report through MTD. This changes how records are kept, how often income is reported, and how the tax year is finalised.

This insight explains what changes, who is affected, and how to prepare.

What Is Making Tax Digital?

MTD requires taxpayers to use approved software to maintain records and submit updates to HMRC. Paper records and manual online forms no longer meet the standard.

Making Tax Digital for Income Tax is a new reporting framework for sole traders and landlords. Instead of one annual Self Assessment return, landlords submit quarterly updates and a year-end final declaration, all through compatible software.

MTD already applies to VAT-registered businesses. The next phase, MTD for Income Tax Self Assessment (MTD ITSA), extends these requirements to individual landlords and sole traders from April 2026.

What Changes from April 2026?

The Income Threshold

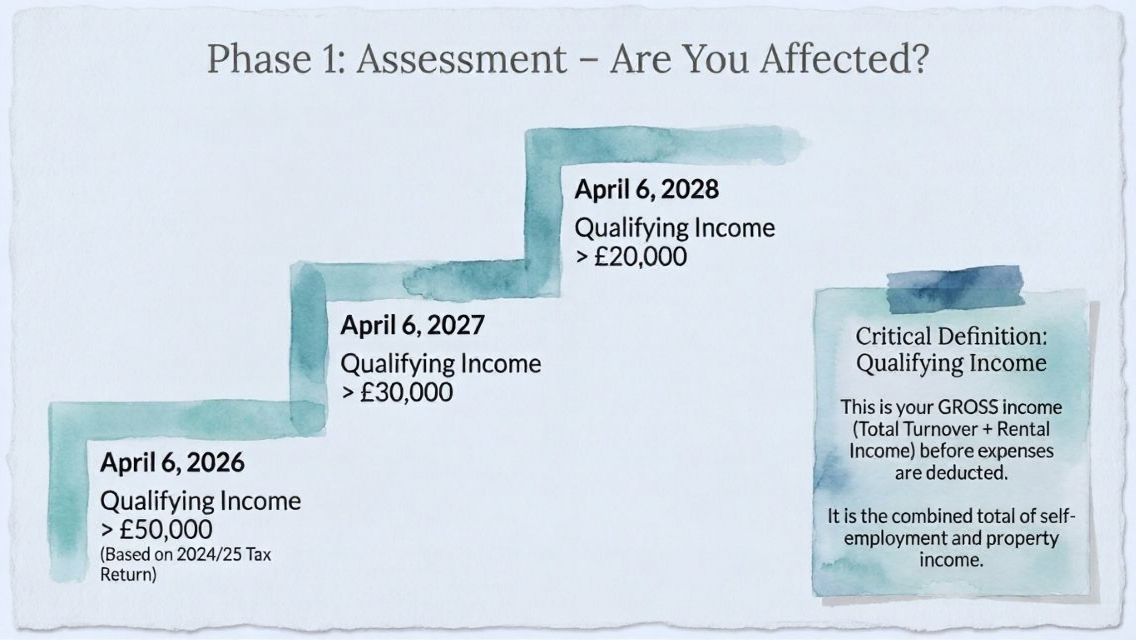

From 6 April 2026, MTD for Income Tax becomes mandatory for individuals whose total gross income from property and self-employment exceeds £50,000 per year.

The threshold is based on gross income before expenses. Only rental and sole trader income count toward it. Employment wages, pensions, and dividends are excluded.

For example: a landlord who received £55,000 in rent but had £15,000 in expenses is still above the threshold. Gross rental income was £55,000. Net profit is not the measure.

The Rollout Timeline

The threshold reduces in subsequent years:

- April 2026: £50,000+ gross income

- April 2027: £30,000+ gross income

- April 2028: £20,000+ gross income (proposed)

Landlords not in scope for 2026 should monitor income levels each year.

Who Is Affected

MTD for Income Tax applies to individual landlords filing Self Assessment returns. It does not apply to limited companies. If you hold rental properties through a company, that company pays Corporation Tax and is not subject to these rules.

The April 2026 changes apply to residential landlords operating as individuals.

What Landlords Must Do Under MTD

Keep Digital Records

Paper-based bookkeeping no longer meets HMRC’s requirements. Every rent payment, expense, and invoice must be recorded digitally in approved software. Records must be kept for at least five years after the relevant tax year.

Some software connects to bank feeds, so transactions import automatically. This removes manual data entry and reduces errors.

Submit Quarterly Updates

Instead of one annual return, landlords submit four income and expense summaries per tax year. Each covers one quarter and is due one month after that quarter ends.

| Quarter | Period | Deadline |

| Q1 | 6 April to 5 July | 7 August |

| Q2 | 6 July to 5 October | 7 November |

| Q3 | 6 October to 5 January | 7 February |

| Q4 | 6 January to 5 April | 7 May |

Quarterly updates are summaries, not tax calculations. They provide HMRC with a periodic snapshot of income and expenses. HMRC may return an estimated tax liability based on what is submitted.

Submit a Year-End Final Declaration

At the end of the tax year, landlords complete a final declaration through MTD software. This replaces the traditional Self Assessment return. It consolidates quarterly updates, allows for adjustments and reliefs, and confirms the year’s totals.

The deadline remains 31 January following the end of the tax year. Tax due is also payable by this date.

A Penalty Points System Applies

HMRC is introducing a points-based penalty system. Each missed quarterly deadline earns one penalty point. Four points trigger a £200 fine. Treat quarterly submissions as fixed operational deadlines.

How to Prepare: A Practical Checklist

Step 1: Confirm Whether You Are Affected

Review your total rental and self-employment income for the 2024/25 tax year. If it exceeds £50,000, you fall within the first group mandated to use MTD from 6 April 2026.

If you are below the threshold, track your income against the lower thresholds planned for 2027 and 2028.

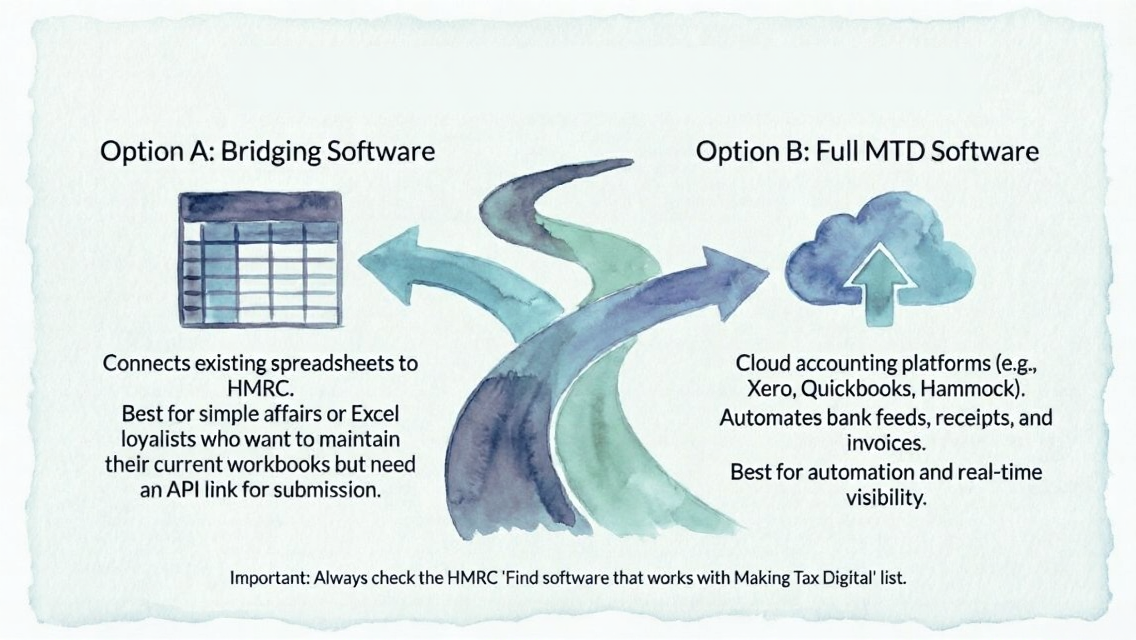

Step 2: Choose MTD-Compatible Software

HMRC does not provide software. You must select a commercial product from HMRC’s approved list. Options include general accounting tools like QuickBooks and Xero, and landlord-specific applications.

When selecting software, confirm it can:

- Handle multiple properties

- Distinguish between rental income and sole trade income

- Connect to bank feeds

- Submit quarterly updates and final declarations to HMRC

Start trialling software well before April 2026. Most providers offer free trials. Use the trial period to input real data and test the quarterly reporting flow.

Step 3: Begin Digital Record-Keeping Now

Do not wait until April 2026 to switch to digital records. Start now. Use your chosen software, or an interim spreadsheet, to log income and expenses for the current tax year.

Build these habits:

- Log transactions monthly or more frequently

- Scan and store receipts digitally

- Reconcile records against bank statements each quarter

By the time the mandate arrives, the workflow will already be routine.

Step 4: Set Quarterly Calendar Reminders

Add the four quarterly deadlines to your calendar now. Set reminders at least two weeks before each deadline to allow time to review and submit.

If you work with an accountant or tax agent, confirm they will handle submissions under MTD. Agents can file on your behalf through MTD software, but must be formally authorised.

Step 5: Prepare Your Workflow

MTD replaces the year-end scramble with four smaller submissions throughout the year. This requires a change to how property admin is structured.

A practical approach:

- Dedicate time each month to updating records

- Use a separate bank account for rental income and expenses

- Check if your software is using the accounting basis (cash basis is permitted only up to £300,000 turnover)

Step 6: Get Support If Needed

An accountant or bookkeeper can manage quarterly filings on your behalf. Some letting agents and property managers are developing MTD support services. Landlord associations such as the NRLA publish guidance and training on the topic.

A Note on Voluntary Opt-In

Landlords below the income threshold can voluntarily register for MTD before it becomes mandatory. Some choose this route to build familiarity with the system before the obligation arrives.

Summary

MTD for Income Tax introduces a structured reporting cycle for qualifying landlords. The transition is operational, not just administrative.

Three things change:

- Record-keeping must be digital

- Income and expenses are reported quarterly

- The year-end return is replaced by a final declaration through software

The April 2026 mandate applies to individual landlords with gross rental and self-employment income above £50,000. The threshold reduces in subsequent years, bringing more landlords into scope over time.

The right preparation is straightforward: confirm your status, choose compatible software, start keeping digital records now, and build the quarterly submission rhythm into your property workflow.

With the right systems in place, MTD becomes routine.

%20for%20Income%20Tax%20Mind%20Map.webp)

HMRC’s countdown is officially on, but compliance doesn’t have to mean chaos. If you’re in the first wave of landlords moving to digital reporting this April, the secret to a smooth transition is starting your preparation now. We’ve put together a readiness kit to help you bridge the gap and stay strategic.

CHALLENGE Yourself – Take a Quiz